Before Thursday’s market motion kicks off, Palantir (PLTR) will ship fourth-quarter financials. Deutsche Bank’s Brad Zelnick expects the outcomes will are available in in line with the information, which requires income of $418 million.

However, the 5-star analyst believes a lot of the investor focus will flip to the “sustainability and quality of growth and any initial view for C1Q22 and CY22.”

Zelnick notes that the slowdown in Government and Commercial income, coupled with “contribution margin compression,” is a worrying signal relating to the long-term alternative and profitability for Palantir.

That stated, after an uncharacteristic 6% drop in C3Q, primarily based on current deal exercise and “healthy reported backlog metrics,” Zelnick is searching for a big quarter-over-quarter uptick in C4Q Government income. While conceding the federal government enterprise is “somewhat lumpy in nature,” the analyst continues to imagine Palantir’s Government alternative is “substantial.” While progress charges are more likely to “moderate,” Zelnick believes the “magnitude of the long-term opportunity remains intact.”

But as has usually been famous about Palantir, the large information specialist generates the majority of its income from authorities contracts, which, whereas massive in nature, means a lot of the gross sales come from just some shoppers. Therefore, it’s seen as important for the corporate to make headway within the industrial section for the enterprise to finally succeed. Here, Zelnick isn’t certain the corporate has what it takes to make the grade.

“Despite some positive signs on new pilots, customer count and deal volume, the flow through to Commercial revenue has been underwhelming thus far,” famous Zelnick, who stays “cautious” on the Commercial facet, believing the chance for Palantir right here is “smaller than many appreciate.” The analyst sees “proprietary platforms” akin to Palantir offering extra of a “niche” service.

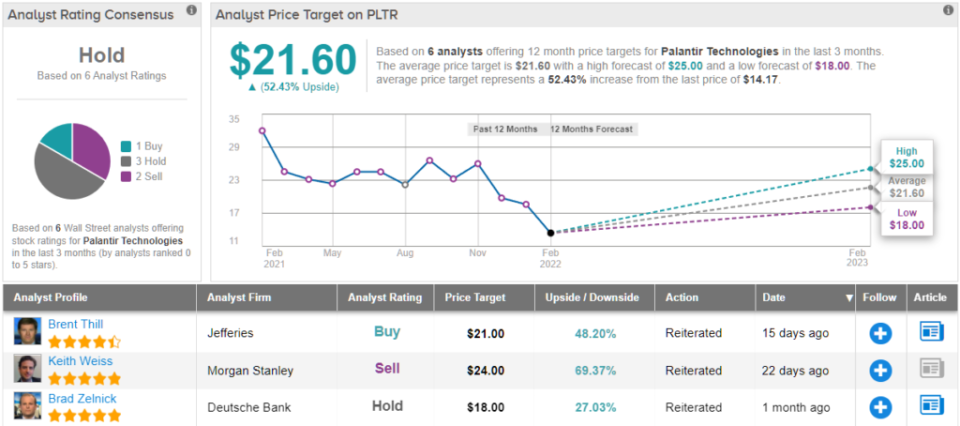

As such, with an “eye toward stabilizing growth and profitability as keys to begin rebuilding confidence,” forward of the print, Zelnick charges PLTR a Hold together with an $18 worth goal. Nevertheless, following the shares’ 60% pullback over the previous 12 months, there’s upside of 27% from present ranges. (To watch Zelnick’s monitor report, click on right here)

Story continues

The remainder of the Street is on the identical web page. Palantir’s Hold consensus ranking relies on 1 Buy, 3 Holds and a pair of Sells. Just like Zelnick’s take, nonetheless, there are many good points projected nonetheless; at $21.60, the common worth goal suggests shares will rise ~52% within the 12 months forward.

It will likely be fascinating to see whether or not the analysts improve their scores or scale back worth targets over the approaching months. (See Palantir inventory forecast on TipRanks)

To discover good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Best Stocks to Buy, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is essential to do your personal evaluation earlier than making any funding.