We noticed one thing of a rally within the markets final week, however was it simply the well-known ‘dead cat’ bounce? A take a look at the charts may counsel that. Since the start of April, we seen two brief rallies in an in any other case bearish development – however the second rally was shorter than the primary, with a decrease peak. Market watchers are beginning to surprise if the cat is finished bouncing.

So, how can buyers journey out this hostile atmosphere?

Goldman Sachs analyst Kash Rangan believes that software program shares, with at present depressed costs and excessive upside potentials can present a measure of safety for buyers looking for a defensive stance in opposition to the bigger market downturn.

“While software is late-cycle and investors are rightly wary of relatively unchanged FY forecasts, we revert to our intrinsic analysis as a backstop to the divergence between these companies’ strong business models and current valuations. We maintain our view that profitable growth software can serve as a defensive asset class during challenging economic conditions,” Rangan defined.

Rangan follows up his dialogue of ‘defensive’ software program shares with two such picks. As famous, these shares characteristic beaten-down share costs however nonetheless have loads of upside potential – in Rangan’s view, higher than 50% for the yr forward. Do different analysts agree with Rangan? Let’s take a more in-depth look.

GitLab (GTLB)

The first of those ‘Goldman software picks’ is GitLab, an innovator in DevOps platform improvement. The firm affords enterprise prospects an open-source platform for devops work, one which guarantees to extend velocity and effectivity in addition to maximizing the end-product’s general return. GitLab’s revolutionary perception was to permit customers and collaborators to contribute to the planning, constructing, and deployment of the platform via the open-source mannequin. GitLab affords this fundamental platform totally free to prospects, who may subscribe for entry to proprietary upgrades and add-ons.

In the 8 years that GitLab has been open for enterprise, the corporate has seen its product develop to a large viewers. The agency has over 30 million registered customers, representing greater than 100,000 corporations and organizations. From this base, there are greater than 2,000 contributors to the open-source code.

Story continues

The firm went public in October of final yr, and closed its first day’s buying and selling at greater than $103 per share. The inventory has fallen since then, and is down 48% from that opening. The share worth decline has come at the same time as the corporate’s revenues have proven constant positive aspects in every of its first three public earnings reviews.

In these reviews, the highest line has risen from $66.8 million to $87.4 million. The most up-to-date, for Q1 of fiscal 2023, was up 75% year-over-year. At the identical time, the corporate’s web loss has moderated, from 44 cents per share one yr in the past to 18 cents within the present report.

Against this backdrop, Goldman’s Rangan lays out an upbeat case for this open-source software program agency, writing: “Taking a deeper look into our income progress assumptions, we gained confidence in GTLB’s means to maintain a powerful top-line progress charge (of over 38%+ over the following three years) and probably attain FCF breakeven quicker than initially anticipated (4Q24 vs consensus estimates of 2Q25).”

“In addition to GTLB providing a best-of-breed platform in a big and under-penetrated $40bn TAM, we see the end result of the next components driving progress: 1) a gentle, elevated NER (>130%) supported by seat enlargement and prospects coming off of discounted subscription plans 2) an growing mixture of Ultimate as the popular pricing tier amongst new prospects, and three) a wider top-of-funnel as corporations get comfy with a streamlined DevOps platform,” the analyst added.

This stance led Rangan to improve GTLB shares from Neutral to Buy, and his worth goal of $80 implies a one-year upside potential of ~51%. (To watch Rangan’s monitor report, click on right here)

The bullish Goldman view is not any outlier right here, because the Strong Buy consensus score on this inventory is unanimous and supported by no fewer than 9 optimistic analyst opinions. The inventory is promoting for $53.14 and its $68.88 common worth goal signifies it has room for ~30% progress within the subsequent 12 months. (See GTLB inventory forecast on TipRanks)

Atlassian Corporation (TEAM)

The second Goldman software program decide we’re taking a look at is Atlassian, an organization working within the B2B realm. Atlassian affords office streamlining software program for enterprise prospects; the corporate’s best-known product, Jira, lets managers and employees contribute collectively to assign, arrange, and monitor office duties. Atlassian affords a variety of different office software program merchandise for quite a lot of makes use of in teamwork and collaboration.

The high quality and applicability of Atlassian’s merchandise could be seen by a easy monitoring of its revenues over the previous couple of years. The firm has seen the highest line develop persistently, regardless of – or maybe due to – the COVID pandemic. When lockdown insurance policies had been in impact, Atlassian’s software program, which helped facilitate distant work, discovered new demand – and saved its expanded buyer base.

In its most up-to-date quarterly report, for the third quarter of fiscal yr 2022, Atlassian confirmed $740.5 million on the prime line. This was up 30% year-over-year, and an organization report for quarterly income. The firm’s web loss within the current quarter, at 47 cents per share, was in keeping with the 48 cents reported within the year-ago quarter.

In current months, Atlassian has been working to switch its merchandise, together with new and current prospects, to the cloud, a transfer that may make it a subscription software program firm on the SaaS mannequin. Atlassian is pushing the transfer as an enchancment in reliability, safety, privateness, and compliance for its buyer base.

Atlassian’s relevant merchandise and rising cloud enterprise, in Rangan’s view, supply a path ahead for the corporate – on a path that’s solely starting.

“With ~226,000 customers and $2.6bn in revenue today, the company has only tapped a fraction of the 2.2mn companies with 10+ knowledge workers and $29bn market opportunity (estimated to grow to $176 by 2025). The availability of a free offering of its products is a competitive advantage for TEAM that allows for steady and strong customer adoption trends with better sales/marketing efficiency,” Rangan defined.

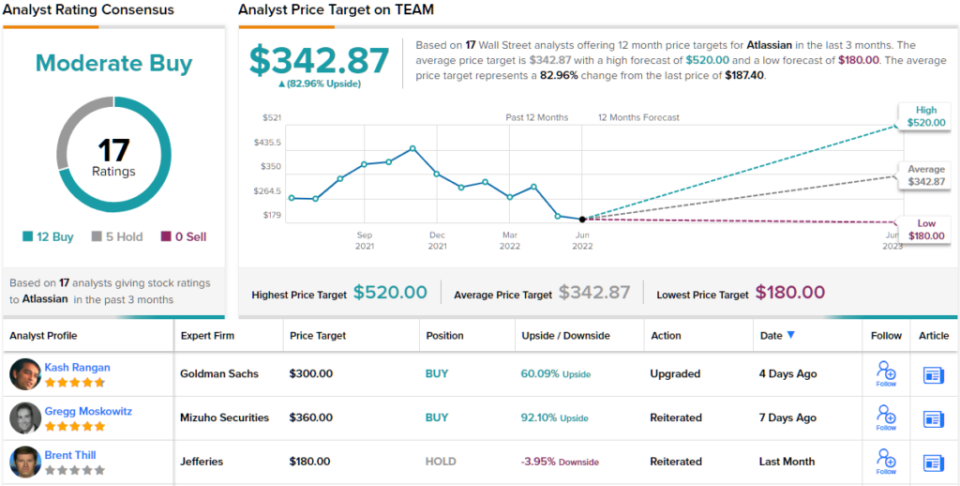

This is one other inventory that will get an improve from the Goldman analyst, who bumps it from Neutral to Buy. Rangan’s $300 worth goal implies an upside of 60% within the coming yr. (To watch Rangan’s monitor report, click on right here)

All in all, this software program agency has picked up 17 current analyst opinions, together with 12 Buys and 5 Holds, giving it a Moderate Buy consensus score. The inventory’s common worth goal of $342.87 suggests a one-year upside of ~83% from the present share worth of $187.40. (See TEAM inventory forecast on TipRanks)

To discover good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is essential to do your personal evaluation earlier than making any funding.