The inventory market has fallen to begin the yr, and a few shares have fallen greater than others. For traders, nonetheless, that brings up alternatives – simply because a inventory has fallen fairly a bit does not essentially make it a foul funding.

The trick for traders is to inform the distinction between shares which can be low-cost at their new low costs and shares which can be actually damaged. That’s the place the Wall Street execs are available.

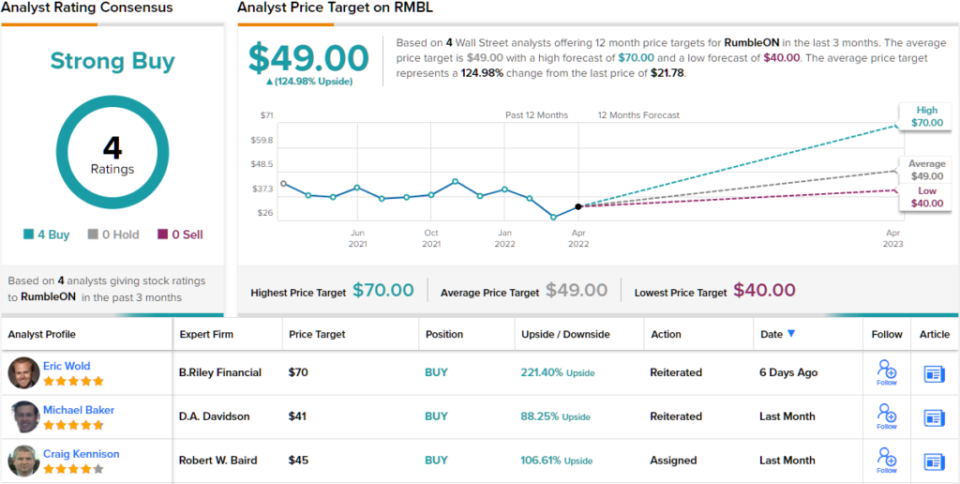

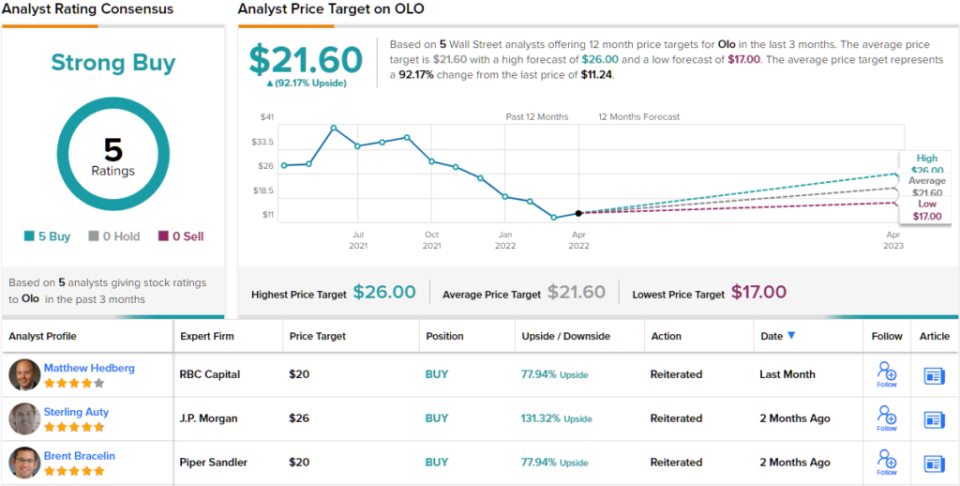

These skilled inventory pickers have recognized two compelling tickers whose present share costs land near their 52-week lows. Noting that every is about to take again off on an upward trajectory, the analysts see a sexy entry level. Using TipRanks’ database, we came upon that the analyst consensus has rated each a Strong Buy, with main upside potential additionally on faucet. Let’s take a more in-depth look.

RumbleON (RMBL)

We’ll begin with RumbleON, a novel automotive-related firm. The firm provides an internet platform to attach patrons and sellers of leisure sporting autos, notably bikes, but in addition pre-owned powersports autos of all kinds. RumbleON’s omnichannel tech-based platform makes it simple for powersports followers to attach, to purchase and promote, with the objective of constructing powersports extra accessible to extra folks.

RumbleON ran web losses by way of most of 2020 and 2021, however in 4Q21 the corporate reported an EPS revenue of $1.35 on web revenue of $20.7 million. This was up dramatically from the $1.81 EPS loss in 4Q20. At the highest line, the corporate confirmed $440.9 million in complete income, up a powerful 47% year-over-year. For the complete yr 2021, the corporate had revenues of $1.58 billion, with an annual web revenue of $45.5 million – these had been report outcomes for a full yr.

During the primary quarter of this yr, RumbleON has been transferring to develop its operations and footprint. The firm acquired Freedom Powersports, a distributor for 15 producers, promoting by way of 13 retail places. The acquisition expands RumbleON’s community to 55 brick-and-mortar places. RumbleON paid $130 million for Freedom, in a transaction composed of each money and inventory.

Story continues

Despite the growing earnings and increasing footprint, RumbleON shares have tumbled 48% this yr.

However, 5-star analyst Eric Wold, of B. Riley Securities, thinks this new, decrease inventory worth may provide new traders a possibility to get into RMBL on a budget.

“We really feel that RMBL shares have been overly punished and supply an more and more enticing alternative buying and selling at 3.4x our 2023 AEBITDA estimate—or a ~38% low cost to the median of the car seller peer group,” Wold opined.

Wold goes on to elucidate why, within the occasion of elevated recessionary pressures, RumbleON will discover itself in a comparatively robust place: “We believe the low inventory levels throughout the segment provide a hedge against that risk for RMBL. In typical recession scenarios, the industry would be facing too much inventory for the reduced demand and this would drive aggressive moves to sell inventory, including heavy promotional activities. However, that should not be the case now with the powersports industry and the RMBL dealer network were a recession to occur as the manufacturers would still need to fill a depleted dealer channel.”

Based on the entire above, Wold charges RMBL a Buy, with a $70 worth goal to counsel an upside of 221% for the subsequent yr. (To watch Wold’s observe report, click on right here)

Wold could also be exceptionally bullish, however the Street is also sanguine about RMBL. The inventory’s 4 latest analyst critiques are all constructive, giving it a unanimous Strong Buy consensus ranking. With a median worth goal of $49, and a present buying and selling worth of $21.78, this inventory has a one-year upside of 125%. (See RMBL inventory forecast on TipRanks)

Olo Inc. (OLO)

The second beaten-down inventory we’re is Olo, whose identify is an abbreviation of ‘online ordering.’ This New York-based cloud software program firm provides a B2B SaaS product, directed to eating places; the platform permits enterprise clients to position orders and direct deliveries, even from a number of suppliers and origination factors.

Olo has been in enterprise since 2005, however solely entered the general public buying and selling markets in March of 2021. Since that IPO, nonetheless, OLO shares have fallen drastically. In 2022, the inventory is down 46%, and total, it’s down 68% from its first day’s closing worth.

The fall in share worth got here whilst the corporate has proven strong earnings and worthwhile EPS in every of the 4 quarterly studies it has launched since going public. At the highest line, revenues have grown from $36.1 million in 1Q21 to $39.9 million in 4Q21; the final two quarters have proven sequential positive factors, and the 4Q high line was up 31% year-over-year. Non-GAAP EPS was regular at 3 cents per share within the first three studies, and slipped to 2 cents within the 4Q report; all 4 met or exceeded the earnings forecasts. On the steadiness sheet, Olo had $514.4 million in money on the finish of 2021.

This rising tech firm caught the attention of Piper Sandler’s Brent Bracelin, a 5-star analyst ranked among the many high 5% of his Wall Street friends. Bracelin writes, “This fall marks the seventh straight quarter of balancing of worthwhile development, which is exclusive for a high-growth small-cap cloud software program mannequin… We proceed to view 1Q22 as a possible development trough as the corporate laps its hardest examine interval, forward of the Q2 reset in DoorDash pricing. That stated, the FY22 outlook of 31% y/y on the midpoint means that top-line development may reaccelerate exiting Q1.”

Bracelin’s feedback help his Overweight (i.e. Buy) ranking on Olo shares, and he provides them a $20 worth goal, indicating his confidence in ~78% upside potential for the subsequent 12 months. (To watch Bracelin’s observe report, click on right here)

That the bullish view is par for this course is evident from Wall Street’s consensus – a Strong Buy, primarily based on 5 unanimously constructive analyst critiques. OLO shares are buying and selling for $11.24, and their $21.60 common worth goal suggests an upside of 92% from that stage over the subsequent 12 months. (See OLO inventory forecast on TipRanks)

To discover good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Best Stocks to Buy, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is essential to do your individual evaluation earlier than making any funding.