contributions will soar practically 10% in 2023, nevertheless it’s not all the time a good suggestion to max out retirement investing")

The federal authorities will permit you to save practically 10% extra for retirement in 2023. But it’s unlikely that many will make the most of the tax break. The easy cause: Most individuals don’t make sufficient cash to save lots of extra from their paychecks.

The common quantity that members contribute is 7.3% of their wage, in response to Vanguard’s How America Saves 2022 report. At that charge, you’d should make greater than $300,000 to hit the $22,500 most quantity an worker can save in a office plan for 2023, up from $20,500 in 2022. To put it one other manner, to save lots of the max, you’d should put apart $1,875 monthly, or $865 per paycheck should you’re paid biweekly.

Only 14% of members saved the utmost quantity in 2020.

Few individuals can even doubtless make the most of the rise within the catch-up contribution restrict, which can permit these 50 and older to contribute an additional $7,500, up by $1,000 from 2022, for a complete of $30,000. Vanguard’s report discovered that solely 16% of these eligible take part, regardless that 98% of plans permit for catch-up contributions.

“The max numbers are very high. A lot of people don’t make that kind of money,” says Anqi Chen, assistant director of financial savings analysis on the Center for Retirement Research at Boston College.

You may not have to max out

Not everybody wants that sort of cash put away for retirement. The key’s to save lots of over time to ultimately be capable of change your present revenue sooner or later, supplemented by Social Security. If you’re making $60,000 now, it wouldn’t make sense to attempt to save greater than a 3rd of your yearly revenue simply because the federal government says you may.

“You don’t want to deprive yourself today or later on. You want to balance that over time, to be able to maintain the same standard of living in retirement,” says Chen.

The tried-and-true technique to get individuals to contribute to retirement financial savings is a financial incentive: matching funds. That “free money” on the desk is on the base of each suggestion for the way a lot staff ought to contribute. Give a minimum of as much as the match, everybody says. But nearly all firm retirement plans supply matching funds, and it hasn’t but solved the retirement disaster going through most Americans who haven’t saved sufficient.

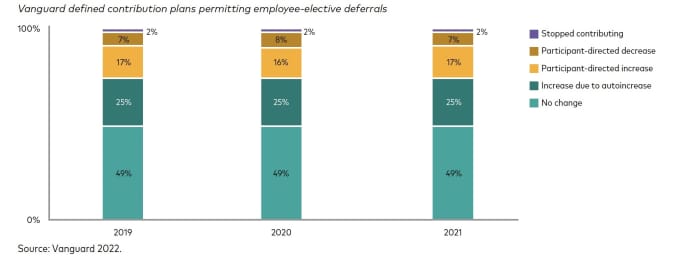

Trend in deferral charge modifications

Vanguard 2022

If there’s a takeaway from the brand new IRS limits, it’s that pushing up the boundaries yearly does assist. Retirement contributions have been listed for inflation since 2001 for good cause, as a result of legislators acknowledged that the quantity you want sooner or later is consistently going up.

Ten years in the past, the utmost for 401(ok) contributions was $17,000 and going again 30 years to 1992, it was $8,728. In in the present day’s {dollars}, that actually wouldn’t be sufficient.

At the identical time, the federal government has to cap it someplace to place a restrict on tax deferral, so you may’t simply shelter all of your revenue from the IRS.

“These annual step-ups matter over time, because saving for retirement is a multidecade thing,” says David Stinnett, head of strategic retirement consulting for Vanguard.

His recommendation for individuals who can’t max out, notably youthful staff, is to a minimum of contribute as much as the corporate match after which mechanically escalate your financial savings charge over time to one thing within the rage of 12% to fifteen%.

It might be useful to consider the quantities in greenback phrases, slightly than percentages.

“By starting small and thinking of it as just ‘3 pennies per dollar’ earned and then adding ‘2 pennies per dollar’ each year going forward, you’ll get on track to those recommended savings rates in no time,” says Tom Armstrong, vp of buyer analytics and perception at Voya Financial.

Escalating over time does appear to maneuver the needle, in response to Vanguard’s examine, a minimum of should you have a look at the speed of individuals coming to the desk. The voluntary participation charge was solely 66%, however the participation charge for automated enrollment was 93%.

“What that does is make it easy to save more,” says Stinnett.