U.S. shares have been sliding on Monday on fears that the current rally was primarily based on a very optimistic view concerning the Federal Reserve’s potential to pivot away from utilizing sharply greater rates of interest to combat inflation.

How are shares buying and selling?

The S&P 500

SPX,

-1.61%

fell 67 factors, or 1.6%, to 4,161

The Dow Jones Industrial Average

DJIA,

-1.35%

shed 438 factors, or 1.3%, to 33,268

The Nasdaq Composite

COMP,

-1.95%

tumbled 260 factors, or 2.1%, to 12,442

On Friday, the Dow Jones Industrial Average fell 292 factors, or 0.86%, to 33,707, the S&P 500 declined 55 factors, or 1.29%, to 4,228, and the Nasdaq Composite dropped 260 factors, or 2.01%, to 12,705. The Nasdaq Composite is up 19.3% from its mid-June low however stays down 18.8% for the 12 months up to now.

What’s driving markets?

Wall Street was on target for chunky declines as traders expressed wariness over a sequence of financial, technical and seasonal components.

The benchmark S&P 500 had rallied sharply off its mid-June low, partly on hopes that indications of peak inflation would enable the Fed to sluggish the tempo of rate of interest rises and even pivot to a dovish trajectory subsequent 12 months.

However, that assumption was challenged final week by a succession of Fed officers who appeared to warn merchants about embracing a much less hawkish financial coverage narrative. Central bankers will collect this week at their annual retreat in Jackson Hole, Wyoming, and Federal Reserve Chairman Jerome Powell is anticipated to ship a extremely anticipated speech on the financial outlook.

“The hawkish argument will prove convincing for Powell and the broader committee. However, the dovish arguments may limit the extent of the hawkish guidance from Powell at this week’s meeting,” famous Citigroup’s analysts led by chief US economist Andrew Hollenhorst. “Likely moderately-hawkish outcomes would involve Chair Powell clarifying that despite policy rates being in the range of ‘long-run’ neutral, appropriate settings are now higher given above-target inflation or Powell simply signaling that policy should be expected to continue to tighten until there are more convincing signs inflation is returning toward target.”

“We do not expect explicit guidance on the size of the September policy rate increase, but we continue to see a 75bp hike at the meeting as likely, even if used-car prices weigh on core inflation again in the August report,” stated analysts in a shopper notice on Monday.

See: Here are 5 causes that the bull run in shares could also be about to morph again right into a bear market

Falling bond yields this summer time helped equities of their current rally. But after dropping under 2.6% at the beginning of August, the 10-year yield

TMUBMUSD10Y,

3.023%

is nearing 3% once more.

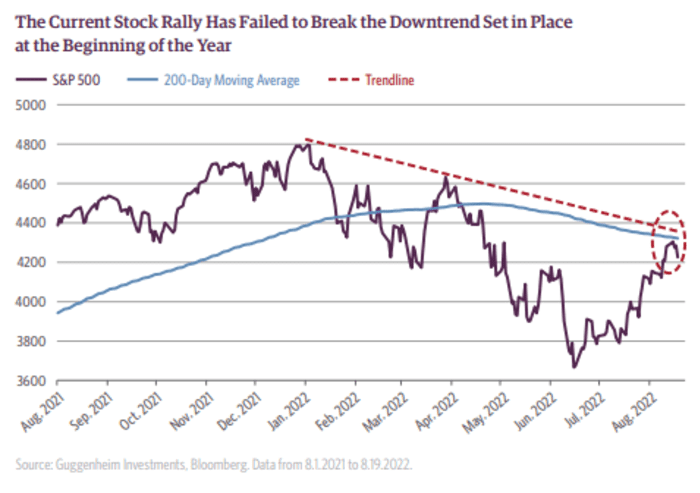

Another subject worrying the bulls is the S&P 500’s failure to interrupt by a key technical stage, elevating fears the market stays in a downtrend. The large-cap index is on tempo for its second consecutive lack of 1% or extra, the longest such streak since 4 buying and selling days ending June 13, based on Dow Jones Market Data.

Source: Guggenheim

“Stocks have seen a strong rally since the Federal Open Market Committee meeting in mid-June, but the S&P 500 has struggled to close above its 200-day moving average in the past week,” stated analysts at Guggenheim in a notice. “Based on the history of previous bear markets, this level (currently 4,320) is an important one to watch. A failure to break the 200-day moving average could portend much deeper losses for equities in the months ahead.”

See: Once providing the worst return on Wall Street, money is now wanting like the very best asset to personal, says Morgan Stanley

The greenback index

DXY,

+0.83%

is again to 20-year highs as worries concerning the European financial system amid surging vitality costs pull the euro

EURUSD,

-1.03%

to parity with the buck. A powerful greenback is related to weaker shares, because it erodes overseas earnings of American multinationals by making them value much less in U.S. greenback phrases.

Still, Lori Calvasina, fairness analyst at RBC Capital Markets, famous that some traders thought “the summer rally in the S&P 500 has left stocks looking expensive again” however she was extra sanguine concerning the market’s prospects.

“S&P 500 P/E’s have moved slightly above average on bottom-up consensus EPS forecasts, and look even more elevated on our own EPS forecasts of $214 (2022) and $212 (2023),” she stated. “But even when we substitute in our own EPS views to the P/E calculation, it’s worth noting that multiples are still decently below the last few major peaks. In our minds, while this is worrisome, it’s not sufficient to call an imminent end to the summer rebound.”

Which corporations have been in focus?

Shares of AMC Entertainment Holdings

AMC,

+3.03%

have been in give attention to Monday as the corporate’s new most well-liked share class is about to start buying and selling beneath the ticker ‘APE’.

Signify Health

SGFY,

+33.00%

shares surged 34% following a Wall Street Journal report saying that Amazon is amongst a number of corporations bidding for the home-health-services supplier. The healthcare firm is on the market in an public sale that would worth it at greater than $8 billion, based on Wall Street Journal.

Travel shares declined with cruise line shares comparable to Carnival Corporation

undefined,

Royal Caribbean Group

RCL,

-3.51%

and Norwegian Cruise Line Holdings

NCLH,

-3.13%

declining by round 3%.

How are different property faring?

The 10-year Treasury yield

TMUBMUSD10Y,

3.023%

topped 3%.

The general risk-off tone out there is impacting most asset courses. Oil futures

CL.1,

-0.94%

have been decrease with U.S. crude down 2% to $89.01 a barrel.

Gold futures

GCZ22,

-0.81%

GC00,

-0.81%

for December supply have been off $17.50, or 1%, to $1,744 per ounce on Comex, because the rising greenback and better Treasury yields continued to weigh on treasured metals.

The ICE U.S. Dollar Index

DXY,

+0.83%,

a gauge of the greenback’s power in opposition to a basket of rivals, was up 0.2% at 108.38, nearing a multi-decade excessive reached final month.

Bitcoin

BTCUSD,

-0.48%

fell 1% to $21,296.

In Europe, the Stoxx 600 fairness index

SXXP,

-0.96%

fell 1.2%, whereas the UK stock-market benchmark FTSE 100

Z00,

+0.07%

was down 0.4%. In Asia most bourses have been additionally decrease, although China’s Shanghai Composite

SHCOMP,

+0.61%

bucked the pattern with a 0.6% achieve after the central financial institution trimmed mortgage charges to help the struggling property sector.